Fiscal and monetary policy in the euro area stand at a crossroads. The rules- based framework established in the 1990s—the Maastricht Treaty and the Sta- bility and Growth Pact—has failed to prevent the steady accumulation of public debt, which now stands closer to 90% of GDP than to the Treaty’s 60% ceiling. Successive crises have pushed member states beyond the fiscal limits, while the European Central Bank has been drawn beyond its original mandate. Large- scale asset purchases and prolonged periods of ultra-low interest rates have compressed sovereign bond yields and eased government financing conditions, weakening the market discipline that once constrained highly indebted states.

These developments expose a fundamental tension at the heart of the euro’s architecture. When fiscal policy lacks credibility, monetary policy is inevitably forced into a role that extends beyond the pursuit of price stability. The euro area therefore faces the risk of fiscal dominance: a regime in which the central bank effectively loses operational independence because it must preserve governments’ ability to finance deficits. The costs are well known—an inflation tax that is regressive in its incidence and corrosive in its effects on price signals, savings and the efficient allocation of capital.

The fundamental problem does not lie in the design of the fiscal rules them- selves. Successive reforms have left long-term debt dynamics largely unchanged. The deeper cause is persistently weak economic growth. Without stronger growth, fiscal consolidation requires adjustments of a scale that no democratic polity can sustain. The path forward lies not in yet another revision of the rules, but in structural reforms at both the national and European levels—reforms capable of unlocking the full potential of the single market. A credible growth agenda is the surest safeguard of the European Central Bank’s independence and its price-stability mandate.

The Savings and Investment Union (SIU) is the right idea at the right time, but it’s already mired in national political opposition. At a policymaking level, SIU remains focussed on technical and supervisory integration. Unfortunately, this approach ignores the most fundamental characteristic of Continental European societies – a deep aversion to risk which is embedded in household behaviour. Yet, tackling this issue is essential to completing a meaningful investment union. But it requires more than a technical or legislative solution. It requires cultural change.

Europe possesses capital in extraordinary abundance — over €10 trillion sits in low-yield bank deposits alone with an annual savings rate approximately three times greater than the US. Italian households and businesses alone save 400 billion euros annually. Culture, not capital, is the problem.

European households, shaped by historical trauma, large welfare states and inert political systems, have developed a deep aversion to productive investment. Until this is confronted directly SIU will always remain less than the sum of its potential parts.

Drawing on relevant research from economics, behavioural finance, sociology and psychology this brief makes five proposals designed to shift the default settings of European households’ financial behaviour. None requires European households to become “American”. But they do require a political and institutional shift that challenge accepted European norms.

The UK’s recent political and economic trajectory offers valuable lessons not only for its own future but also for Europe’s. While Brexit is often cited as the defining factor in the UK’s challenges, the deeper story lies in structural economic pressures and how these have reshaped the country’s political landscape. This policy brief examines the UK’s key economic difficulties, how these have fractured the electorate and what implications this dynamic holds for Europe, particularly France and Germany, where mainstream parties face similar vulnerabilities. Greece’s recent recovery is explored as a counter-example, illustrating how credible reform and institutional stability can rebuild both market confidence and political legitimacy.

Affordability has moved to the centre of the political debate. Citizens have been plagued by the post-Covid inflationary experience. Gas prices skyrocketed following Russia’s invasion of Ukraine. And even if headline figures have come down now, past inflation remains stored in current prices.

Some have been hit more heavily than others. If you only had a small financial buffer before, that buffer has now gone, or you are only getting by on credit. Food prices, energy prices and the cost of housing impact you much more, because they constitute a much higher share of your spending.

The affordability crisis is one of the main drivers of the continued rise of right-wing authoritarian parties. As anti-system parties, they profit from anger and disillusionment. Their electorate is composed, to a greater than average extent, of the less educated, those with lower incomes, the unemployed and blue-collar workers. Members of these groups experience competition for scarce public services and housing during events of mass migration such as those provoked by Russia’s aggression against Ukraine or the bombardment of Syrian cities.

We are witnessing the revolt of the lower middle class.1 The traditional social–democrat responses of increasing state spending and taxation have lost credibility in the eyes of the voters. Looking at their electorate, the authoritarian right has managed to form new workers’ parties by promising a reduction in social competition through very strict migration policies or ‘remigration’ and the limitation of global economic exposure.

The Martens Centre’s Academic Council has asked some of its eminent experts to develop new ideas on affordability from a Christian Democratic and conservative perspective. We focus on the housing market (Eoin Drea), energy poverty (Dimitar Lilkov) and digital equality (Žiga Turk), as well as on how to enable an economic turnaround (Ann Mettler), with precise recommendations for policymakers.

Europe’s declining productivity growth has become a central constraint on long-term prosperity. For over two decades, productivity gains have weakened across most EU Member States, while the gap vis-à-vis the US and leading Asian economies has widened. Recent flagship reports—the Letta Report on the Single Market and the Draghi Report on Competitiveness—show that Europe’s competitiveness challenge is structural, persistent, and urgent.

While low investment, fragmented markets, and slow innovation diffusion are well known, one part of the problem lies in Europe’s missing independent scientific advisory capacity on productivity and competitiveness as the basis for evidence-based policymaking. Structural reforms often require long time horizons, cross-policy coordination, and political resolve beyond electoral cycles. Yet EU and national policymaking often remain biased toward short-term measures and legislative output rather than economic outcomes. Addressing Europe’s productivity challenge requires better policies and corresponding policy advice institutions at the European level.

Research shows that independent, scientifically grounded advice improves policymaking. Advisory institutions diagnose trends early, develop long-term reform frameworks, filter flawed proposals, and translate evidence into actionable policy. They also inform public debate and strengthen accountability by making trade-offs transparent.

Politically, such institutions can make a difference: policymakers often postpone reforms with long-term benefits while prioritising visible short-term measures. Independent bodies embed long-term economic reasoning and highlight the economic costs of inaction. Effectiveness increases when advice combines independence with visibility through clear communication and public engagement.

National Productivity Boards without a sister institution at the EU level

National Productivity Boards (NPBs), established following the 2016 Council Recommendation, have improved evidence-based policymaking by analysing productivity trends, competitiveness drivers, and reform needs.

However, no EU-level institution currently aggregates NPB findings or translates them into coherent EU guidance. This limits the value of the NPBs, as many of the challenges they identify are European rather than national: energy market fragmentation, incomplete capital and digital markets, missing cross-border infrastructure, and uncoordinated innovation funding cannot be solved by Member States alone.

In addition, stronger coordination and harmonisation of the NPBs as independent scientific advisory bodies could pay off in terms of comparability and impact at the national level. Currently, their institutional designs differ in independence, resources, data access, and visibility; weak legal anchoring and unstable funding further constrain effectiveness.

Draghi’s warning: Europe is losing speed

Mario Draghi has highlighted Europe’s investment and innovation gaps and criticised slow policymaking, regulatory uncertainty, and a lack of strategic prioritisation. Legislative activity is rewarded, while policy effectiveness and learning from failure receive little recognition. Weak evaluation mechanisms and limited independent scrutiny allow ineffective policies to accumulate raising costs and undermining competitiveness.

A European Productivity Board: strengthening independent scientific advice at the EU level

A European Productivity Board (EPB) would complement national boards and establish independent scientific policy advice at the EU level by aggregating NPB analyses, producing EU-wide assessments of productivity trends and competitiveness, identifying structural bottlenecks and reform priorities, and contributing to the harmonisation of NPB methodologies and data.

The EPB should be independent, composed of a rotating committee of European experts supported by a permanent analytical secretariat, with transparent appointment procedures, financial autonomy, and full publication rights. It should advise the European Commission while reporting to the European Parliament, reinforcing accountability and remaining outside day-to-day policymaking in order to provide unbiased ex ante advice, rigorous ex post evaluations, and monitor of the implementation.

A pragmatic step towards a more competitive Europe

Europe’s productivity challenge is no longer a question of diagnosis but of action. National Productivity Boards have contributed to improving evidence-based debate at the Member State level, yet many of the binding constraints on productivity—such as market fragmentation, weak diffusion of innovation, energy market inefficiencies, and regulatory complexity—are fundamentally European in nature. A European Productivity Board (EPB) would add clear value by aggregating national evidence, harmonising methodologies, and translating fragmented diagnoses into coherent, EU-wide policy guidance.

Crucially, the EPB would embody a qualitatively different mode of policymaking: insulated from day-to-day political bargaining, institutionally anchored, and explicitly mandated to adopt a long-term perspective that electoral cycles and administrative incentives routinely undermine. Experience shows that structural reforms are often delayed, weakened, or abandoned as a result of vested interests and entrenched status-quo biases. Ultimately, productivity-enhancing reform hinges on political will. However, such will rarely materialises spontaneously. Sustained, evidence-based awareness generated by an independent scientific body that delivers credible, transparent, and comparable analysis of Europe’s structural bottlenecks—while clearly identifying actionable policy pathways at the EU level—can reshape public debate, empower reform-oriented policymakers, and increase the political cost of inaction or purely symbolic policies. By reporting publicly and to the European Parliament, an EPB would not supplant democratic decision-making; it would reinforce it by providing policymakers and citizens with a robust analytical foundation to challenge entrenched interests and translate long-recognised reform priorities into effective, implemented policy.

Hence, establishing a European Productivity Board represents a pragmatic and timely institutional innovation, aligned with a reform-oriented and competitiveness-focused vision for Europe’s future.

A longer version of this article will be published in European View soon.

Andreas Reinstaller Tobias Thomas Competitiveness Economy

The EU enters 2026 facing – once again – its economic reality. Low growth, relatively good employment numbers, public debt inching upwards and an expanding list of new spending priorities. As for much of the last two decades, the bloc’s economic fundamentals remain stubbornly mediocre.

We all know the story of Europe’s current geopolitical crunch. The war in Ukraine has exposed Europe’s strategic dependencies, from energy to semiconductors. The real problem – currently overlooked – is that addressing these vulnerabilities requires sustained economic resources that current growth trajectories simply cannot provide.

Defence spending commitments ring hollow when public finances are already stretched and resistance to structural reform remains entrenched across member states. Even something as basic as Europe’s Banking Union (stalled since 2014) is still subject to rancour and division at member state level.

The uncomfortable truth Brussels refuses to acknowledge is that security and economic performance are inextricably linked. A Europe that cannot generate robust economic growth is a Europe that cannot fund its own defence, let alone project power beyond its borders.

Borrowing solves some immediate shortfalls, but it’s not – as history has shown us repeatedly – a long-term solution for financing the long-term expansion of a military base.

The political landscape makes matters worse. Populist movements across the continent have successfully weaponised economic stagnation, linking legitimate concerns about living standards to divisive cultural narratives. Mainstream parties have responded with a mix of solutions that have only partially addressed the underlying frustration driving voters toward the extremes.

The European middle classes, squeezed by housing costs, the rising cost of living, and economic insecurity, are losing faith in the European project’s ability to deliver prosperity. For the younger generations, the economic challenges increasingly feel insurmountable.

This is not an abstract problem for 2026 but a concrete political crisis that will play out in national elections and EU negotiations in the months and years ahead.

Consider the practical implications for key policy debates. The Green Deal imposes significant costs on European industry at precisely the moment when global competitors face no such constraints. Without a credible strategy to maintain industrial competitiveness during this transition, many European manufacturers will simply not survive.

Some of the EU’s regulatory initiatives – if not adjusted – risk handicapping European companies in sectors where scale and innovation matter decisively. Europe’s approach to economic policy too often seems designed for a world where European markets are large enough to dictate global terms. Unfortunately, this is a world which no longer exists.

What makes 2026 particularly consequential is the convergence of immediate pressures with longer-term structural challenges. An aging population means healthcare and pension costs are rising just as spending on defence must rise significantly. The artificial intelligence revolution threatens to displace millions of European workers while the continent struggles to produce global AI leaders.

Even in this post-internet AI age – Europe remains overly dependent on a traditional banking sector that remains fragmented and undercapitalised compared to American competitors.

These problems are well versed, and the solutions well known.

Usually this is the part of the article where the author extorts European leaders to embrace deepening the single market – particularly in services and the capital markets – as a way of heralding a new golden age of integration (and growth).

Alas, in an EU which can’t even agree to accept a trade deal with the Mercosur economies, further market integration will likely resemble a torrid process of half-measures. Think the acrimony of the global financial crisis from 2008, not the euro-enthusiasm of the late 1990s.

That’s because Europe first needs a cultural shift, even before political progress can take place.

Europe – western and southern continental Europe in particular – are trapped in a low-risk, low-reward strategic outlook. It’s a stability first model which was perfectly understandable in 1950, but wholly out of touch with 2026 realities. That’s why low growth is the new normal in Europe’s biggest economies and why public debt is rising to unsustainable proportions.

The role of the state has now become so large – and so indebted – that the allocation of risk and the financial burdens in society have become skewed. So, while the Italian government chokes under 3 trillion euros of debt (!), its households are among the richest in Europe with incredibly high savings levels and low debt. Simultaneously, its entire social security system is predicated on protecting the benefits of the older generations, while the young struggle and emigrate.

As a result, Europe is now full of very rich countries, with very poor, debt-filled governments.

French unwillingness to accept any notable pension reforms is a baguette-sized symbol of Europe’s fractured strategic thinking.

To generate real growth requires a fundamental reshaping of Europe’s social economic model. Meaningful economic expansion requires financial incentives at national level to better utilise existing cash reserves. Social security models need to reflect demographic realities and housing models overhauled to give younger people a chance to match (and exceed) the social standing and wealth of their parents.

Most fundamentally, European leaders need to explain honestly to voters that competitiveness requires difficult choices about labour markets, business regulation, and public spending priorities. 2026 will reveal whether Europe’s political class possesses the courage to make these choices or whether they will continue to substitute grand rhetoric for genuine reform.

Europe doesn’t need to chase the American model. It has more than enough wealth and capacity to develop its own distinctive approach. But without more risk – and more economic growth – Europe’s defence is doomed.

On January 3, 2026, the United States carried out major strikes in the Venezuelan capital of Caracas and its vicinity, before capturing the country’s illegitimate ruler, Nicolás Maduro, and flying him to the United States to face federal criminal charges, including narco-terrorism and drug trafficking. Following his capture, Venezuela’s Vice-President, Delcy Rodríguez, was sworn in as acting President.

The vast majority of Venezuelans supported the American operation, after 12 years of a brutal Maduro regime. During his tenure, Venezuela lost roughly 70% of its GDP, reducing 80% of its population to poverty, with 50% of those suffering from extreme poverty. Thousands of companies and farms were expropriated. Those that survived were suffocated by price controls, currency controls, production quotas, and arbitrary enforcement. The Venezuelan economic crisis since 2013 is considered the worst economic performance of any country in the modern times in the absence of a war.

In addition to this stunning economic collapse, Venezuela suffered a profound political breakdown. Under Maduro’s rule, elections were consistently stolen and manipulated to maintain power rather than reflect the will of the people. The last example of this was in the 2024 Venezuelan presidential election, when the National Electoral Council declared Maduro the winner despite credible evidence that his opponent, Edmundo Gonzalez, secured a clear majority. Since the 2000s, the Venezuelan regime stacked the courts with loyalists, disqualified opposition leaders, jailed critics, and violently suppressed protestors.

However, any exultation from Venezuela’s people must be tempered by the fact that this operation is just the beginning; the decisions taken in the coming days will determine Venezuela’s future. The real test now is whether the country can translate the removal of a dictator into the restoration of the rule of law, credible governance, and economic freedom, without allowing a power vacuum to generate further instability.

Building a Transition Path

Building a successful transition depends on sound decisions across institutions, but none of these decisions can take root without effective security on the ground. Venezuela today remains an extremely high-risk environment. Irregular armed groups, drug trafficking networks, organised crime, and foreign hostile actors, including Iranian-linked cells, operate with relative impunity across large parts of the country. Without credible protection against these actors, there can be neither sustained economic recovery nor free and fair elections. Markets cannot function, investment cannot flow, and democratic processes cannot be trusted when violence, intimidation, and sabotage remain unchecked.

Security mechanisms must therefore prioritise the protection of civilians, but also of the people tasked with rebuilding the Venezuelan state. This includes technical experts, energy specialists, public administrators, and investors who will necessarily need to operate on the ground, many of whom will come from abroad. If these individuals face credible threats to their safety, the reconstruction of the oil sector, public institutions, and the broader economy will simply not occur. This is why a sustainable transition requires a structured partnership between the United States, a legitimate transitional government, and Venezuelan society itself.

Once a baseline of security is re-established, Venezuela must move immediately to economic normalisation. This means lifting price and currency controls, gradually unifying exchange rates, restoring basic monetary credibility, and reopening trade and investment flows with democratic partners. The energy sector must be opened to private investment, so that Venezuela can become an energy hub once again. In the past two decades, Venezuela has lost over 70% of its oil production. From producing 3.5 million barrels per day, Venezuela is now producing less than a million. Returning to its previous levels will require $60 billion in investment and roughly a decade.

In this context, the European Union can emerge as a particularly credible and economically rational partner for Venezuela’s recovery. Europe combines three assets that are directly aligned with Venezuela’s post-crisis needs: surplus capital, advanced industrial and energy technology, and a growing strategic imperative to diversify away from Chinese-controlled supply chains. The European economy runs a persistent current account surplus and faces structurally weak domestic investment demand, creating strong incentives to deploy capital abroad in projects with long time horizons and real asset backing. Venezuela, by contrast, offers a rare combination of scale and underutilisation. It has the largest proven oil reserves in the world, substantial natural gas potential, and an energy system in need of comprehensive rehabilitation.

From a political perspective, Europe should participate in Venezuela’s transition efforts. Yes, the risks are real. Venezuela is fragile, its institutions are weak, and criminal structures remain embedded in the state. But there is no reward without risk, and risk aversion is not a policy. In Venezuela, every peaceful option was tried and exhausted. Years of mass protests. Repeated participation in elections that were systematically manipulated. Diplomatic pressure, mediation efforts, and sanctions. None of it worked. The regime adapted, hardened, and increased repression. Standing with Venezuelans will not be cost‑free, but it is the only choice worthy of Europe’s values and interests. If European governments commit to this difficult transition alongside Venezuelan society, a country that once stood as a democratic and economic beacon in Latin America can be restored. A stable, free Venezuela will matter not only to its own citizens, but to the wider geopolitical balance and global security architecture of the coming decades.

Jorge Jraissati Economy Foreign Policy Latin America

The European Union has a growth problem. Its share of the global economy has been on a steady decline for decades, dropping from over 20 per cent in 2000 to around 15 per cent currently. In part, this is due to catch-up growth in developing countries but the EU has also lagged behind its peer across the Atlantic, the United States. Europe’s productivity growth, rate of innovation and ability to foster new, innovative companies all compare unfavourably with the US.

At the same time, the EU is operating in an increasingly difficult external environment. Russian aggression has led to increased energy prices as well the need for increased defence spending, putting strain on public purses that were already under pressure from high debt levels, mediocre productivity growth and higher health and pension spending as populations age. Meanwhile, the US has turned increasingly protectionist and has broken with WTO rules, forcing the EU to accept higher tariffs. China, on the other hand, has been an aggressive competitor, putting increasing price pressure on European products, both in the European domestic market and export markets.

The first step towards solving a problem is acknowledging its existence. In that respect, Europe has done well, with not one, but two major reports coming out last year by former Italian prime ministers Enrico Letta and Mario Draghi. These reports do a good job laying out the productivity challenge and the various ways the EU can address them. However, many of their proposals are politically very ambitious, and face resistance from member-states that are loath to give up additional powers to the EU. For instance, the banking and capital market unions are long-standing projects that would provide obvious benefits for the EU but have made little headway against national opposition. Similarly, the issuance of EU bonds has been limited to exceptional circumstances such as the pandemic, and although European financial markets would clearly benefit from an EU-level safe asset, there is little chance of this happening in the near future.

This paper provides a reform agenda that would boost economic growth while also being politically feasible within current political constraints. By focusing on a few key issues – better regulation, energy, a savings and investment union, and the single market for services – we hope to provide a trigger for practical action that would leave Europe better able to foster the growth it needs.

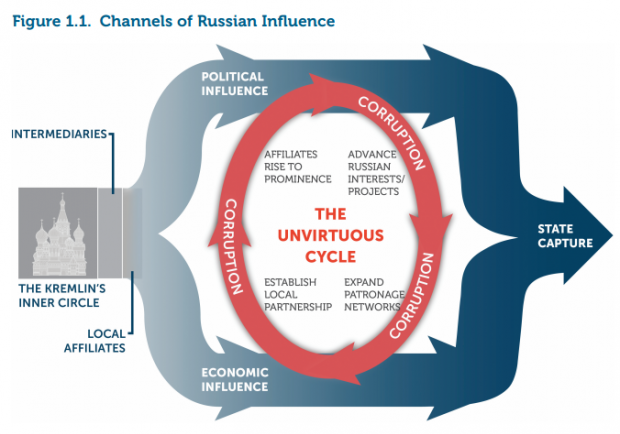

For Vladimir Putin, China became the major economic lifeline since the beginning of Russia’s full- scale aggression against Ukraine in 2022. Chinese goods and technologies replaced lost access to Western technology imports, whereas Russian commodities banned by Western democracies flooded the Chinese market, providing Russia with much-needed export revenue. Both countries hold regular high-level summits, never missing an opportunity to stress the essentiality of their partnership to building a new, post-Western and post-democratic world.

However, underneath the PR surface of pompous summits and aggressive public promotion of a “no limits” partnership, clear constraints to a full-scale economic partnership emerge. China doesn’t seem to be interested in investing in Russia, in bailing the country out from its current economic woes, in sharing technology, and, more generally, in supporting Russia’s emergence as a competitor in the manufactured products markets. Russian producers also complain about competition with Chinese goods at the domestic Russian market, which has recently led to introduction of tough tariff barriers like a recycling fee for cars. Vital Russian commodities like coal or wheat face import tariffs or outright import bans in China. China doesn’t provide Russia with loans much needed to solve Russia’s budget and investment crises. Most of the major mutual projects, for which implementation was announced in the recent years, have been scrapped or are not really moving forward, with only a few exceptions.

To what extent are these problems complicating and limiting the development of Sino-Russian economic partnership? The current study considers these issues in more detail.

If you wish to watch our Thinking Talks interview with Vladimir Milov, discussing this paper and more, click here.

A Summary of the Findings of an Online Study Carried out in France, Germany, Italy, Poland, Romania, Spain and Sweden

Understanding how EU citizens perceive working migrants is important for policymakers aiming to manage migration both from within and without the bloc. An online study commissioned by the Martens Centre in 7 EU countries shows that despite being preselected to achieve a balance of views on migration in general, most respondents across the countries surveyed expressed positive views about the economic contributions of those migrants who are working. Also, irrespective of their general views on migration, a large majority of respondents believe that migrant workers fill jobs that the locals do not want to perform, as opposed to taking jobs away from natives. There was a split across political values, with a large proportion of respondents with supranational values expressing the belief that working migrants contribute positively to the national economy, while among those with national values only a smaller majority did so. On average, a small majority of participants felt positive about general government policies to encourage labour immigration, although beliefs on this matter varied significantly between countries.

To read the original technical report by Verian, click here.

As the largest European political party, the EPP has the responsibility and capacity to shape the future path of the European Union. The Union, standing at a crossroads, needs a strong compass and clear vision of Europe as a strong global actor, grounded in its values, to regain the trust of European citizens.

The Martens Centre has developed the following recommendations that address six key policy fields for Europe’s future: defence, competitiveness and growth, migration, demography, climate change, and resisting the extreme right. Based on a concise description of the challenges, the Martens Centre proposes concrete and decisive steps for the current legislative term.

Climate Change Defence Democracy Demography Economy European People's Party Migration

This report analyses the economic agendas of right-wing populist parties (RWPPs) in Europe, plus cases from the UK, US, and Argentina. Across eleven dimensions, it compares their positions on economic policies. RWPPs harness discontent with liberal globalisation and socio-economic change but lack a unified doctrine. They mix ideas with nationalism and opportunism. Most back private ownership and SMEs; calls for nationalisation is rare and limited to critical infrastructure. Regulation ranges from deregulation to state protection of “strategic” sectors.

Some RWPPs pair expansive welfare talk with “welfare chauvinism,” reserving benefits for natives and curbing labour migration. They advocate for tax cuts for low- and middle-income individuals, resist tax harmonisation and wealth taxes, and often accept higher debt. In finance, they reject deeper European capital-market integration and assert monetary and fiscal sovereignty. On trade and the EU, they oppose multilateralism and denounce Brussels’ overreach.

Migration is the clearest common denominator, framed instead by culture and security than by shared economic beliefs. Many oppose the euro and digital currencies. Climate scepticism is widespread, notably the European Green Deal.

Overall, RWPPs remain market-based but seek nationalist re-shaping—especially in trade and integration. The message for centrist parties is clear: renew the social market economy, address middle-class insecurity, and make the Single Market fairer.

The spectacular – yet not totally unexpected – collapse of Francois Bayrou’s government is the latest chapter in a political quagmire that has dogged France ever since Emmanuel Macron’s centrist bloc failed to secure an absolute majority during the 2022 legislative elections. The impasse devolved into a full-blown crisis in 2024 when the French President—bewilderingly—called a snap election, yielding the most fractured Parliament in modern French history.

Yet fragmentation alone need not have made the country ungovernable. Unfortunately, France lacks a tradition of coalition governing that solves this issue in other Western democracies. But the true issue lies beyond politics: France has become hopelessly addicted to living beyond its means and financing this excess through debt. The only way out would be for a significant portion of the country’s political class to look French voters in the eye and tell them it’s time to get off the gravy train.

Needless to say, this crisis isn’t going anywhere nice.

France has consistently spent more than it raises in revenue since the early 1970s. As its debt continues to rise (now 114% of GDP), Paris will find it harder to sustain its increasing debt servicing costs. A vicious spiral that is exacerbated by anaemic growth (0.6% projected for 2025) and the highest proportion of public spending relative to GDP (57%) in the entire EU. Paris now pays more than Athens when borrowing on the financial markets. Remarkably, France now spends more every year paying interest on its colossal debt than it does on defence.

Although some political leaders have shown a commitment to bringing France’s public finances under control, notably Interior Minister Bruno Retailleau, the loudest voices are those of the extremists; both Jean-Luc Mélenchon’s LFI and Marine Le Pen’s RN call for repealing the recent reform which raised the retirement age to 64 (from 62, with LFI even saying it should actually be lowered to 60). This stunning proposal comes even though life expectancy is at a historic high, and the cost of pensions is spiralling out of control and will only get worse given the top-heavy nature of France’s demographic pyramid. France’s situation is uniquely bad because of its bloated state and chronic overspending. It is also impressive because of its current political woes. But while the root cause is not unique to France, the fact that France is the second largest economy in the Eurozone means its lack of economic credibility on debt reduction could have potentially ruinous implications for other Euro members.

And just to be clear – France currently has no credible plan for reducing its deficit. Forget a balanced budget, French policymakers can’t even agree on a framework to get the budget deficit down to 3% by 2030.

The broader lessons for the rest of the Eurozone (and the EU) are clear. High taxes and low growth are a threat to European welfare as a collective. Europeans should view recent events in France as a warning and take a hard look at how they can stabilise their balance sheets. This is especially vital as exogenous pressures from Russia and other hostile actors will necessarily mean an increase in defence spending, at the expense of other areas, at least until growth can be revitalised.

For politicians, it is also vitally important to acknowledge how the constraints imposed by high public debt impact other vital societal priorities such as education, health and housing. Yet, France remains an incredibly wealthy European state with very considerable financial reserves. French households alone hold over 600 billion euros in Livret A, the most common savings accounts in the country, while gross domestic savings total over 20% of GDP.

France’s problem isn’t a lack of money – it’s a decades-long ritual of concentrating debt at the public level. Public spending which is no longer sustainable.

France is not the “New Sick Man of Europe”; it has simply caught the worst case of a common ailment. To save the patient, let’s follow the science: cut unproductive, runaway spending and instead focus on delivering growth.

Eoin Drea Theo Larue Crisis Economy EU Member States

Building EU Resilience Through Strategic Complementarities

As significant global players in the semiconductor industry, Malaysia and Taiwan are connected by a high degree of economic complementarity. They both rely on a complex supply chain, in which Europe has an important role to play. While still catching up in the chip industry, the EU must project itself as a stable, innovation-driven, and value-aligned semiconductor partner to Malaysia and Taiwan. Driven by a shared interest to boost resilience, the EU and member states must invest strategically in regional dynamics in ASEAN, capitalise on trends shaping the global semiconductor arena, and understand Taiwan’s crucial role in securing resilient supply chains.

The Trump administration’s aggressive use of financial sanctions and threats has laid bare a critical vulnerability: Europe’s economic security is at the mercy of US structural power. This continued exploitation highlights a staggering analytical failure in Europe, where banking and finance are rarely seen as geopolitical domains. In March new US Secretary of the Treasury, Scott Bessent, acknowledged that 40%–50% of his role is national security. By contrast, how many of us can recall the last time a European finance minister discussed the centrality of money in our national security decision-making? Europe’s dependence on US-controlled financial systems demands urgent attention.

In the eurozone, ‘banks’ accept demand deposits, offer credit and process payments, unlike credit institutions (credit-only) or payment providers (transactiononly). Large ‘direct participant’ banks access T21 for real-time settlements, while smaller ‘indirect participants’ rely on them, creating access dependencies. These regulated financial activities, deposit-taking being the most stringent of all, shape a system where most institutions outsource banking to cut costs, amplifying reliance on a few gatekeepers with direct access. This structure exacerbates vulnerability to dominance, a leverage the US has wielded for decades in pursuit of political ends.

This policy brief analyses how US control over financial choke points undermines Europe’s strategic autonomy. It examines and reveals the frailty of assuming unfettered financial access will always be there. It explores how the US’s reach, coupled with banks’ risk-averse behaviour, restricts Europe’s policy options, threatening economic and national security ambitions. Without robust, indigenous financial alternatives, the continent risks being forced to bend to Trump. Finance continues to be a huge blind spot for economic security, receiving almost no attention from government officials more focused on which goods we buy and sell, but not how we pay for them. Europe must re-examine the status quo to understand the interplay between banks and non-banks.

To counter this vulnerability, Europe must pursue strategic financial autonomy, defined as the condition whereby European actors can operate free from foreign coercion and sovereign entities can reliably implement policy through financial channels without external interference, a goal this brief advances through targeted recommendations. These include building a more resilient financial ecosystem, promoting euro-denominated liquidity and mitigating extraterritorial legal risks to ensure Europe’s policies are not subject to external vetoes or negation.

Last week, the European Commission unveiled its “Competitiveness Compass”, a long-term roadmap designed to strengthen Europe’s economic resilience. It rightly identifies innovation, energy affordability, and reducing strategic dependencies as core priorities for the EU’s future. The strategy makes a compelling case for cutting red tape, boosting industrial innovation, and aligning green policies with economic growth.

But one fundamental challenge is conspicuously underdeveloped: Europe’s growing labour shortages and demographic crisis.

The EU’s global competitiveness is not just about technological leadership or regulatory efficiency – it is about people. Without a sufficient workforce, no level of innovation, investment, or regulatory streamlining will be enough to sustain long-term prosperity. Yet, the Competitiveness Compass fails to address the need for a coherent, urgent response to the continent’s labour shortages. If the EU does not act now, its workforce crisis will become the single biggest obstacle to achieving the economic vision set out in this new strategy.

The Workforce Crisis is an Economic Crisis

Europe’s labour shortages are no longer sector-specific problems—they are becoming a systemic constraint on growth. The OECD Talent Attractiveness Index consistently shows that the EU underperforms in attracting high-skilled talent compared to the U.S., Canada, and Australia. Meanwhile, Eurostat projects that the EU’s working-age population will shrink from 65% today to just 54%-56% by 2070.

These demographic trends are not just statistics – they are existential threats to European competitiveness. A shrinking workforce means fewer innovators, fewer skilled professionals in key industries, and increasing pressure on social systems. Already, major sectors such as healthcare, engineering, and digital industries are struggling to fill positions, while rural regions face severe depopulation and economic stagnation.

Despite recognising the need for a skilled workforce, the Competitiveness Compass does not treat labour shortages as an immediate crisis. This is a major oversight. Without serious interventions, the EU’s economic model will become unsustainable – not because of lack of investment or industrial policies, but because there simply will not be enough workers to power its growth.

If the Competitiveness Compass is to truly safeguard the EU’s long-term economic future, it must elevate labour shortages and demographic decline as core pillars of its strategy. As outlined in this Martens Centre policy brief, addressing these challenges requires three bold policy shifts:

1. A Talent-Centred Migration Strategy

Europe’s migration policies are not designed for global competition. While Canada and the U.S. actively recruit high-skilled talent, the EU remains bureaucratic, slow, and fragmented.

To address shortages, the EU should:

Create a streamlined EU-wide Talent Visa, similar to Canada’s Global Talent Stream, reducing work permit bureaucracy for high-demand sectors.

Expand Talent Partnerships with key non-EU countries to attract skilled workers in tech, healthcare, and engineering.

Harmonise recognition of foreign qualifications to allow non-EU professionals to fill gaps faster.

The Competitiveness Compass mentions talent attraction, but without serious structural reforms, Europe will continue losing skilled workers to other, more attractive global destinations.

2. An Aggressive Upskilling & Reskilling Strategy

The Competitiveness Compass calls for more investment in innovation, but it does not adequately address the workforce skills gap.

A truly competitive Europe needs:

A European Digital and Green Jobs Academy, providing fast-tracked training for workers transitioning into high-demand sectors.

Stronger public-private training partnerships, ensuring businesses are actively investing in workforce development.

A pan-European mobility programme for upskilling and reskilling workers across borders.

Without a bold upskilling push, the EU risks investing in high-tech industries that lack the skilled workers needed to sustain them.

3. A European Demographic Strategy – Not Just a Workforce Fix, But an Economic Necessity

For years, European policymakers have avoided serious conversations about demographics. This must change. If the EU wants sustainable competitiveness, it must recognise that a shrinking workforce is an economic crisis.

The EU should:

Create a European Demography Fund, supporting policies that encourage family formation and regional revitalisation.

Introduce tax incentives for working parents and support family-friendly workplaces.

Align demographic policies with economic goals, ensuring that Europe remains both a top destination for skilled workers and a place where families thrive.

If Europe fails to address its long-term demographic decline, no amount of investment in competitiveness will compensate for a workforce that simply isn’t there.

The EU Needs a Workforce Compass

The Competitiveness Compass is a step in the right direction, but without a clear strategy for addressing labour shortages and demographic decline, it lacks a solid foundation. A strong, resilient, and innovative Europe cannot thrive without a workforce to sustain it.

If the EU truly intends to remain a global economic leader, it must prioritise talent, skills, and demographic renewal as core pillars of its competitiveness agenda – not afterthoughts. The clock is ticking. The question is no longer whether Europe can afford to act, but whether it can afford not to.

After a grandiose first week (back) in office, President Trump 2.0 has turned international politics upside down, again, leaving governments and analysts alike scratching their heads. Among the flurry of threats and accusations, some of his most foreboding has been directed towards his neighbours to the North.

Even before his inauguration, President Trump has repeated false claims against the United States’ kindred ally, and warned of a tariff hike of 25% on all Canadian imports as early as February 1st. The reasoning behind his Northern fixation remains ambiguous, given that he has harped on just about everything: Canada playing a major role in the U.S. fentanyl crisis (it doesn’t – seizures of the deadly drug along the shared border amount to 0.2% of the volume compared to the U.S.-Mexico border); toting the U.S. healthcare system’s over Canada’s (Canada’s is free); and airing his grievances at the World Economic Forum, where he complained that Canada is “very nasty” on trade (Canadians, nasty? Fake news).

A quick recap, in case he’s forgotten; the overarching Canada-U.S.-Mexico Agreement (CUSMA/USMCA) was negotiated by his own administration, in June 2020. Even so, Trump doubled down by criticising the bilateral trade relationship by, surprise, surprise, making another false claim that the U.S. runs a $200 billion USD deficit with Canada. According to the Office of the U.S. Trade Representative, the U.S. deficit with Canada was only $53.5 billion in 2022, and has been declining since. Furthermore, it is worth noting that this deficit is largely caused by the U.S. importing a significant share of low-cost Canadian crude oil, which helps keep U.S. gas prices lower.

Should he move forward with the tariffs, Canadian officials have already signalled that they are prepared to reciprocate dollar-for-dollar. This dispute could therefore get very ugly, and may reshape the U.S.-Canada relationship in the years to come. As it stands, from security, to the economy, very few countries are so intertwined and interdependent. To offer an example, parts for North American vehicle assembly can cross the shared borders as many as seven or eight times before the finished product is completed.

In the event of a severe trade war with the U.S., Ontario’s political leadership has warned that as many as 500,000 jobs in the province alone could be at risk. Given the weight class disadvantage, Canada would be faced with few options: renegotiate CUSMA/USMCA early, which could be Trump’s intended end game, or risk companies revaluating the costs of running their factories there in light of a possible tariff hike. There is another economic weapon in Canada’s arsenal, however, its nuclear option – energy.

The United States is Canada’s largest consumer of both its oil and natural gas. In fact, continental energy security is one of the very foundations on which the U.S.-Canada relationship was formed. Canada should therefore be prepared to enact export tariffs on its energy or even threaten to limit supply.

This too would not be without risks. On the contrary, it could in fact lead to shortages of oil and refined fuels in other regions of Canada. This is because a significant portion of Canada’s oil pipeline from where it originates in Alberta, travels through the U.S. on its way to eastern Canada, meaning the U.S. has the ability to obstruct Canada from supplying itself. This would of course violate a longstanding treaty, but remember who we’re talking about. After all, tariffs in general are a violation of CUSMA/USMCA.

Should President Trump decide to pursue this path, turning a trade war into an oil war by switching off the taps from Western to Eastern Canada, the hardship would be especially felt in the economic hub of Ontario. These disruptions to Canada’s supply could be overcome eventually through a number of means, but it would be a challenging road ahead and shortages would be a real possibility.

Moving forward, Canada should look to expand the supply capacity of its existing Trans Mountain Expansion (TMX) pipeline to the West Coast, thereby increasing its supply capacity to Asian markets. It should also revive the intra-Canadian pipeline that would enable Canadian oil and fuels to travel east without ever leaving the country. Eventually, this would also open the door for completing a new pipeline to the East Coast, and on to European markets.

Such scenario planning would be unfathomable a few years ago, given the intimate, historic partnership between Canada and the United States. But then again, it is also profound for a sitting U.S. president to attempt to extort or threaten the annexation of its northern neighbour. Given the current political uncertainty, diversification of Canada’s energy exports, and trade relationships, a move away from interdependence with the U.S. seems to be the only guarantee for Canada to retain its economic security. This would also open new opportunities for job creation, new ventures, and markets.

In the weeks and months to come, any potential trade war launched by the U.S. against Canada (and Mexico), should be watched closely by Europe, and all Western nations, really. President Trump’s affinity with the “America First” mantra, after all, means just that. How far he’s willing to extort America’s closest allies to achieve it, will be the question.

For Canada, and Mexico, these threats could be intended to force premature negotiations of CUSMA/USMCA, to avoid possible economic bumps in the leadup to the U.S. midterms, when the agreement is scheduled for review. It could be an attempt by President Trump to negotiate better access to the geostrategic Arctic region via Canada, and coincide with his fixation with Greenland. Or, it could be a move to encourage North American businesses to relocate to the United States.

The bottom line? For the next four years at the very least, the rules-based order, free trade, and norms will not be found in the U.S. playbook. Any leverage will become key in future negotiations, whether we’re speaking of this dispute, or any other involving the U.S. under President Trump.

In the event of an all-out economic war with the U.S., Canada will persevere so long as it invests in its future as a means to ensure its economic security. It should be prepared to use all tools available to its advantage, lessen interdependence with the U.S., and strive for greater autonomy. Indeed, there may be severe economic hardships ahead for Canadians depending on how far this dispute gets. Fortunately, for Canada, no two issues unite the nation more than hockey, and threats to its national sovereignty.

The digital euro project is a reaction to citizen preferences shifting towards payment via digital means. It addresses the fragmentation of the European payment sector with the aim of highlighting ways to support the single market, strategic autonomy and the monetary sovereignty of the EU. Because the digital euro is a complex project requiring a thorough legal, economic and political assessment, this policy brief looks at three crucial aspects of the proposal.

The brief first presents the essential features of the digital euro project in the context of European law, economics and politics. In contrast to private forms of electronic money that private banks create, the digital euro will be a retail central bank digital currency. As such, it will be a direct liability of the central bank, like cash. With many payments moving online, the digital euro ensures the role of public money in an increasingly digitised economy.

This digital euro legislative framework should ensure trust by guaranteeing privacy, access to cash and financial inclusion. The establishment of a digital euro has the potential to cause structural changes to the banking system. Thus, it will need to have carefully calibrated holding limits and will not be remunerated—that is, like cash, interest rates will not be applied.

Third, the policy brief identifies critical aspects, such as the distribution of competences between the lawmakers and the European Central Bank, that require thorough legal, economic and, ultimately, political assessment. Policymakers face difficult questions that ultimately relate to the European Central Bank’s exclusive competence over monetary policy, central bank independence and the relationship of these issues to the structure of the financial system. The brief concludes by offering a series of recommendations for policymakers.

The economic narrative surrounding the European Union (EU) in 2024 was dominated by the publication of the Draghi and (to a lesser extent) the Letta reports.

Both laid bare the challenges facing the EU in a more competitive global economy. Draghi and Letta – directly and indirectly – identified the lack of political action in implementing structural reforms as integral to Europe’s declining global competitiveness.

In many respects the recommendations of these reports were both obvious (more investment!) and based on policies that have been kicked around the Schuman roundabout longer than its ongoing redevelopment (Capital Markets Union!).

Remarkably, it’s like Brussels forgot the quarter of a century since the Lisbon Strategy and Europe’s last great push for growth and jobs.

And therein lies the problem of EU economic policy.

Because long before the pandemic and Russia’s invasion of Ukraine, the economic essentials which drive Europe’s wealth creation were ignored by Brussels-based policymakers. The objectives of deepening the Single Market, completing the Eurozone’s (unfinished) architecture and ensuring Europe is a profitable place to do business were sidelined.

These “boring” topics were replaced by a vision of the EU as a geopolitical actor. A unified world player funding everything from a green-rush transition, pan-European pandemic support, Ukraine and a myriad of other geopolitical “actions”.

A steady stream of constant communication to service Brussels’ expanding communications game.

After all, the Single Market isn’t exactly clickbait compared to visions of global relevance.

And while many of these ambitions remain laudable, the fact is that Europe’s economy is no longer generating the economic growth sufficient to deliver these policies. Joint borrowing is a recipe for further fragmentation without the structural reforms necessary to deliver (not promise!) increased economic growth. Worse still, the avalanche of regulations and directives from Brussels has strangled the growth prospects of European companies.

Large or small, exporting or selling locally – European firms are struggling to invest, expand and grow.

Yet, still, the EU doesn’t full grasp the economic realities. And unfortunately, the examples are almost endless.

Imposing billion of euros (in fines) on EU carmakers for not meeting EU environmental rules is not based on economic realism, nor any rational cost benefit analysis. It’s more centralised state planning than social market economy. Rather, it just makes European companies more vulnerable to Chinese and US competitors while simultaneously costing jobs across the EU.

France – whose inability to observe Eurozone financial rules was long ignored by the European Commission – is now stuck in a high debt, low growth cycle with no politically plausible strategy for reducing its budget deficit. Ironically, only Draghi’s 2012 pledge for the ECB to do “whatever it takes” has prevented France’s financial crisis from spreading to a much more serious European one.

But, that’s not a long term strategy. And for Europe’s centre right the danger signs are everywhere.

Dominating the European Parliament, the College of Commissioners and holding the Presidencies of the Commission and Parliament infers a pressure to deliver.

The warnings have already been delivered. The European Elections of 2024 witnessed a significant increase in parliamentary representation in those hostile to the wider European integration process. In the United States, the detachment of the Democratic Party from its working class (and minority) roots resulted in the return of President Trump and his unique blend of pseudo-conservative populism. His success has further strengthened anti-EU forces across Europe.

The reality is that when families are struggling to pay the bills, to buy or rent a decent place to live and finding their wages always lagging inflation – then the broader environmental or cultural wars just have to wait.

Economics trumps ideology. Every single time.

So what strategy should the centre right seek to own?

Very simply – the return of meaningful economic growth and rising real wages should be the dominant objective.

But to achieve this requires – in many sectors – the EU to do considerably less, not more.

Rules and laws must be simplified. The Single Market must be prioritised and the Eurozone’s architecture strengthened. The EU must enforce its fiscal rules without favour, no matter the size or scale of the member state involved.

But the reality is that the prospects are only mixed at best.

Brussels’ dreams of a Capital Markets Union are stuck facing the reality of entrenched national interests in Berlin and other capitals. Yet here the possibility of real change approaches. A new centre-right-led German government must support the easier movement of capital around the Single Market as an essential element of economy recovery. A Europe that only grows in the North and East will never be a real global player, nor a particularly wealthy one.

The next one hundred days will set the tone for the next four years.

Because, this time, it really is the economy or bust for Europe’s centre right.

Since its inception, the Martens Centre’s project The 7Ds for Sustainability has catalysed interest, fostered dialogue and spurred action. However, as both European politics and global challenges continue to evolve at a rapid pace, we must redouble our efforts. With a new European Parliament and Commission at the helm, the stakes are higher than ever. The interconnected crises—geopolitical tensions, divided societies, climate change, inequality, and the urgent need for competitiveness and prosperity—demand a bold and unified strategy.

I am therefore pleased to present the extended version of the Martens Centre’s strategic document.

The 7Ds for Sustainability: Extended offers a timely and insightful roadmap for navigating this complex landscape. This comprehensive policy book was born out of the collaborative efforts of the Martens Centre research team—under the guidance of Klaus Welle, Chairman of the Martens Centre Academic Council and former Secretary General of the European Parliament—and a group of renowned external experts. The book provides a nuanced and actionable framework for addressing the pressing issues of our time.

The publication outlines seven policy areas: decarbonisation, defence, democracy, demography, de-risking globalisation and digitalisation. These form the bedrock of a more resilient, equitable and prosperous EU. Each chapter provides a comprehensive analysis of the specific challenges and opportunities within these domains, offering actionable policy recommendations to guide the EU’s future trajectory.

I commend the authors for their thoughtful analysis and their commitment to finding solutions that can benefit both present and future generations. By embracing the principles outlined in this book, policymakers, businesses and civil society can work together to create a more sustainable future for the EU.

I am confident that this publication will serve as a valuable resource for policymakers, scholars and the European public alike, inspiring and guiding our collective efforts towards a more sustainable future. The 7Ds for Sustainability: Extended is more than just a set of principles: it is a catalyst for change and action and provides a much-needed compass for navigating the challenges and seizing the opportunities that lie ahead.

Have an inspiring read!

Mikuláš Dzurinda, President of the Martens Centre

Former Prime Minister of Slovakia

Climate Change Defence Democracy Demography Digital Economy EU Member States Foreign Policy Leadership Migration

Debt is a question of dose. Too much, and you lose your political independence and sovereignty. Too little, and you might miss out on the possibility and necessity of building infrastructure that facilitates future development.

Keynes taught us that there are situations in which price and interest signals do not work and, as a result, the state is the only actor able to step in temporarily and stabilise the economy—and with it, the political system. A hard lesson was learned in the 1930s. It inspired us during Covid, when the economy threatened to come to a standstill. But debt was put on the EU’s balance sheet without corresponding own resources for the Union to finance and repay it. In addition, no proper parliamentary oversight of debt at the EU level was introduced.

Unfortunately, we have now entered a period of vulgar Keynesianism: increasing the debt-to-GDP ratio in crisis times and in good times as well. The consequence is a debt-to-GDP ratio of about 90% in the eurozone and around 100% in the UK and the US. If this trend continues, it will not be very long before a debt crisis reoccurs and the independence of our political decision-making is threatened, together with the cohesion of the EU.

China and Japan are no exception to this trend. Japan has already demonstrated how ageing societies, with correspondingly meagre growth, can enter into decades of exploding debt. China’s debt is largely out of control, especially on the local and regional level, for which the central state will ultimately have to take responsibility. This accumulation of debt was partially driven by the end of a property building boom and significant over-capacity in many sectors of the economy. This has resulted in Chinese debt levels no longer being accompanied by a sustainable growth model.

The situation is further aggravated by the fact that public investments have become unavoidable in digital infrastructure, defence and decarbonisation, and to alleviate the financial burdens of unfavourable demographics. De-risking from China will add to the burden. The time of imported deflation that was the consequence of hundreds of millions of Chinese workers being integrated into the global market for the first time seems to be over.

During the eurozone crisis, we learned that cutting expenditure on its own is not the answer, because the potential reduction in debt can be largely offset by a significant reduction in GDP as well. Any successful strategy will therefore have to focus on growth and productivity-enhancing strategies at the same time.

Apparently, populism now comes in both good and bad varieties! Taxing the rich or the super rich – nobody knows where to draw the line – is in the camp of the good. And quick wins in public assent are guaranteed. Unfortunately, a sense of moral superiority and simple-mindedness should not replace rational economic thinking. And even from an ethical point of view, these demands don’t stand firm.

In arguing against these revenant proposals, the most recent one by oxfam, we don’t use the usual counterarguments such as capital always finding ways and loopholes of evasion. These technicalities could be largely solved if there is enough political will to take coordinated action among OECD or G20 countries, which remains dubious given the experience of OECD members trying to harmonise and exchange data amongst themselves. More importantly, the question of taxing wealth is a matter of justice and economic efficiency.

Admittedly, global wealth distribution has become even more unequal than income distribution despite remarkable progress in lifting millions out of poverty across the globe. One of the reasons is that, for decades, we have also seen an almost unceasing shrinking of labour income in national GDPs. It is further indisputable that inequality remains a major obstacle to individual and societal development as well as effective governance.

But these observations lead, if carefully analysed, to consequences other than increasing taxation for the super-rich. Firstly, against the popular assumptions, inequality is not, per se, unjustified. Despite centuries of debate, there is no consensus about “just” distribution of wealth and income. Across countries, there is a wide range of inequality that is not immediately considered unjust by the respective societies. How could any global solution of redistribution by taxation work without conflicting with these deeply rooted national traditions and values?

Secondly, even if we concede that extreme inequality is detrimental, the effectiveness of taxing the rich and super-rich as a solution to remedy these deplorable developments is inconclusive. As a means of redistributing primary income, taxation is, in many cases, the least efficient way to counter inequalities and enable sustained improvement of livelihoods. Price signals are far more efficient in indicating scarcity and adjusting individual behaviour. This is even true for common goods, such as those related to environmental protection.

Thirdly, given the need for global taxation of ultra-high value income to avoid tax evasion, we are far from any entitled supranational actor to do so. Even the European Union, with an already impressive set of genuine competencies, is struggling with receiving any substantial revenues of its own. Next to defence, taxation remains the last resort of national sovereignty. Tapping into super-rich assets would have to happen on a national basis. But then, who will decide how to distribute these potential revenues? Are nation-states really willing to go into another round of global redistribution or would they rather darn their budgetary holes? Aren’t we always complaining about overregulation and bureaucracy, only to theorise about creating another complex system?

There are better ways to address inequality and contribute to a socially fairer distribution. But these measures don’t create sexy political messages or quick fixes, and come along with real hard work for lawmakers, without any immediate reward.

First, the well-known inherent shortcomings of the existing taxation systems should be addressed first and foremost, starting from implicit tax increases through inflation to an overdue transaction tax on digital markets. Simplifying tax declarations and reducing excessive tax deductions are also essential to creating a fairer and more transparent system.

Second, the real injustice is not the tax evasion of several thousands of super-rich. The real social scandal is stripping the middle classes of their ability to take care of their own future and degrading them into becoming recipients of redistribution – not quite what a citizens-based, democratic society should be as it undermines social cohesion and poses risks to the future of democratic values.

Third, broadening the taxation basis through sustainable value-creation should be the real long-term objective. Why are we so obsessed with tax evasion, and capital moving abroad? Because we have not been able to create attractive investment options inside our countries, for instance by encouraging innovation and creating a more balanced economic landscape through a more equal distribution of capital. Questions surrounding the equitable distribution of capital income, especially among employees, must be at the forefront of our policy discussions. Simplistic narratives of taxation and redistribution often fail to address these underlying issues, highlighting the need for a more nuanced discourse.

Fourth, why have we failed for decades to distribute capital income more equally and make it a relevant source of income, e.g., among employees? These are relevant questions. Simplistic narratives of taxation and redistribution often fail to address the issues they purport to solve and require a more nuanced discourse.

The call for quick “solutions” like taxing the rich and super-rich is alluring. However, more effective solutions against social inequality have to address the complexities of our taxation systems and the limits of international coordination. We have to aim at empowering the middle class and fostering an environment conducive to sustainable value creation.

The three largest economies in the Euro are all going nowhere fast. Their declining prospects reflect their deep structural issues. They also symbolise the fragility of a Eurozone which has failed to significantly strengthen its institutional architecture over the past decade.

Quite predictably– the Euro, once again, is hopelessly exposed to domestic financial crises.

All the furore in Brussels about improving EU competitiveness is predicated on a stable currency union. Unfortunately, this assumption will be tested by the financial markets in the months ahead.

And this time it’s the very heart of the EU – France, Italy and Germany – that pose the biggest threats to the Euro’s very survival.

France presents the most immediate problem with a current budget deficit of over 6% projected for 2024. The proposed French budget for 2025 – despite significant tax rises and spending cuts – only envisages Paris reaching the 3% Maastricht criterion by 2029. And even the achievability of this target has been met with scepticism by many economists. With public spending at 58% of GDP and an expanding debt pile approaching 120% of GDP – France is finally facing an economic reckoning decades in the making (Paris hasn’t run a budget surplus since 1974).

The fragility of the Barnier government compounds the nervousness of the financial markets. It now costs France more to borrow money on the financial markets than either Spain or Greece. French bonds are already priced as part of the “euro periphery”. As the Eurozone’s second largest economy the implications of a French financial crisis for the Euro are obvious. As highlighted by the Martens Centre in May 2024, France and Greece are now trending in exactly opposite directions when it comes to debt sustainability.

Similarly, Italy has failed to break out of its low growth, high debt economic cycle. The latest data from the Bank of Italy projects growth of just 0.6% in 2024. The European Commission estimates that its debt will exceed 140% of GDP in 2025. To plug current budget gaps, the Italian government is planning on imposing additional taxes on banks and insurers. Like France, this is not a coherent plan for the public finances, but rather an annual exercise in crisis management.

Germany – despite a very healthy debt to GDP position – is now experiencing the result of decades of underinvestment across key economic sectors. A domestic policy position that is now compounded by an economic model rendered partially obsolete by strategic decisions in Moscow and Beijing. Germany’s current recession may be the harbinger of a truly painful (and lengthy) economic readjustment to come. One that will reverberate throughout Central and Eastern Europe given the integrated nature of supply chains in this region, particularly in automotive production.

The reality of this low growth model is that the Eurozone remains susceptible to a potential French or Italian financial crisis in the short term. A crisis likely sparked by future political instability.

So, while Brussels debates Draghi’s longer term proposals – or the marginal recent revision of the EU’s fiscal rules – the foundations underpinning the Eurozone’s fragility go unaddressed.

Namely – in an unfinished monetary union where the ECB acts as a buyer of last resort for Italian and French debt – there will never be sufficient political ownership to undertake the required national reforms. We shouldn’t forget that the structural impediments to faster growth in both France and Italy – lack of competition in key sectors, unsustainable social security models, local and national level bureaucracy, poorly targeted public spending – are domestic level issues requiring domestic level solutions.

True competitiveness can’t be imposed in a top-down manner on national economies.

France and Italy are only a Eurozone problem due to the possible contagion effects in a partially built monetary union. And because the EU – in ignoring its own “no bailout” rule during the Great Financial Crisis – has de facto embedded “bailouts” into the Eurozone’s institutional structure. So while Draghi may have saved the Euro in 2012, his institutionalisation of the ECB as the ultimate arbiter of national borrowing yields (in effect capping yields by buying available debt) has disempowered national policymakers. It has also ensured the survival of the low growth, high debt model evident in France and Italy over the past decade.

But all is not yet lost. An overarching EU focus on competitiveness, empowering SMEs and reducing bureaucracy should be matched by structural reforms at national level to create a new momentum for action. Returning to the Lisbon Agenda of the 2000s should put the focus on a deepening Single Market as the driver of higher economic growth. EU funding must act as a catalyst for reform at national level, not just a top-up for national budgets. And, perhaps most importantly of all, the EU and member states must stop talking about completing a Banking and Capital Markets Union – and actually deliver. This time, the future of the Eurozone may be at stake.

Environmental degradation is a fact. The prevailing scientific consensus is that humankind is directly responsible for most of the rising carbon dioxide emissions in the atmosphere and their related negative effects. Within the EU political mainstream, these findings have positively resonated in policy and resulted in the most ambitious climate agenda globally. Most European citizens also recognise the threats of climate change and the need for our society to adapt and move in a more sustainable direction.

Decarbonisation is one of the most important political challenges of this century. The goals that have been set for European carbon neutrality by 2050 are laudable but presuppose the mobilisation of huge financial and material resources, as well as fundamental changes in the economic, industrial, transport, agricultural and energy sectors of European states. Climate spending already dominates the EU’s Multiannual Financial Framework (MFF) and the post-Covid recovery fund, with hundreds of billions of euros earmarked for the transition. The European Green Deal has a direct bearing on the economic performance of member states and private enterprises, while also becoming ever more present in the lives and pockets of European citizens.

Importantly, the clean energy transition has a direct impact on the EU’s competitiveness and geopolitical clout. Consider the complexity of implementing such a transformative effort in concert with the rest of the international actors, which have all the incentives to free-ride on the efforts of others or delay the transition away from fossil fuels as long as possible.

The decarbonisation destination is set, but the policy routes are many and uncertain. Regrettably, the EU is in a completely different financial and geopolitical position compared to 2019, when the European Green Deal was announced. We already see clear signals that the current framework is neither generating ‘green growth’ nor putting the continent on a fast track towards carbon neutrality. If the EU is serious about its decarbonisation pledges, it needs to rethink its approach.

This paper has two main objectives. First, it briefly addresses the main shortcomings of the Green Deal—the economic costs of the transition and the effect on European energy security and resource scarcity. It also looks into the overly optimistic projections for the renewable energy rollout and the huge investment gap in decarbonisation. More importantly, it puts forward a number of policy recommendations for European policymakers in the new legislative period. Achieving carbon neutrality should remain the long-term goal, but the policy arsenal has to be improved. The European centre–right needs to be actively involved in leading this strategy by crafting a blueprint that is both realistic and achievable and that is shaped by its own vision and political values.