Related publications

-

Policy Briefs

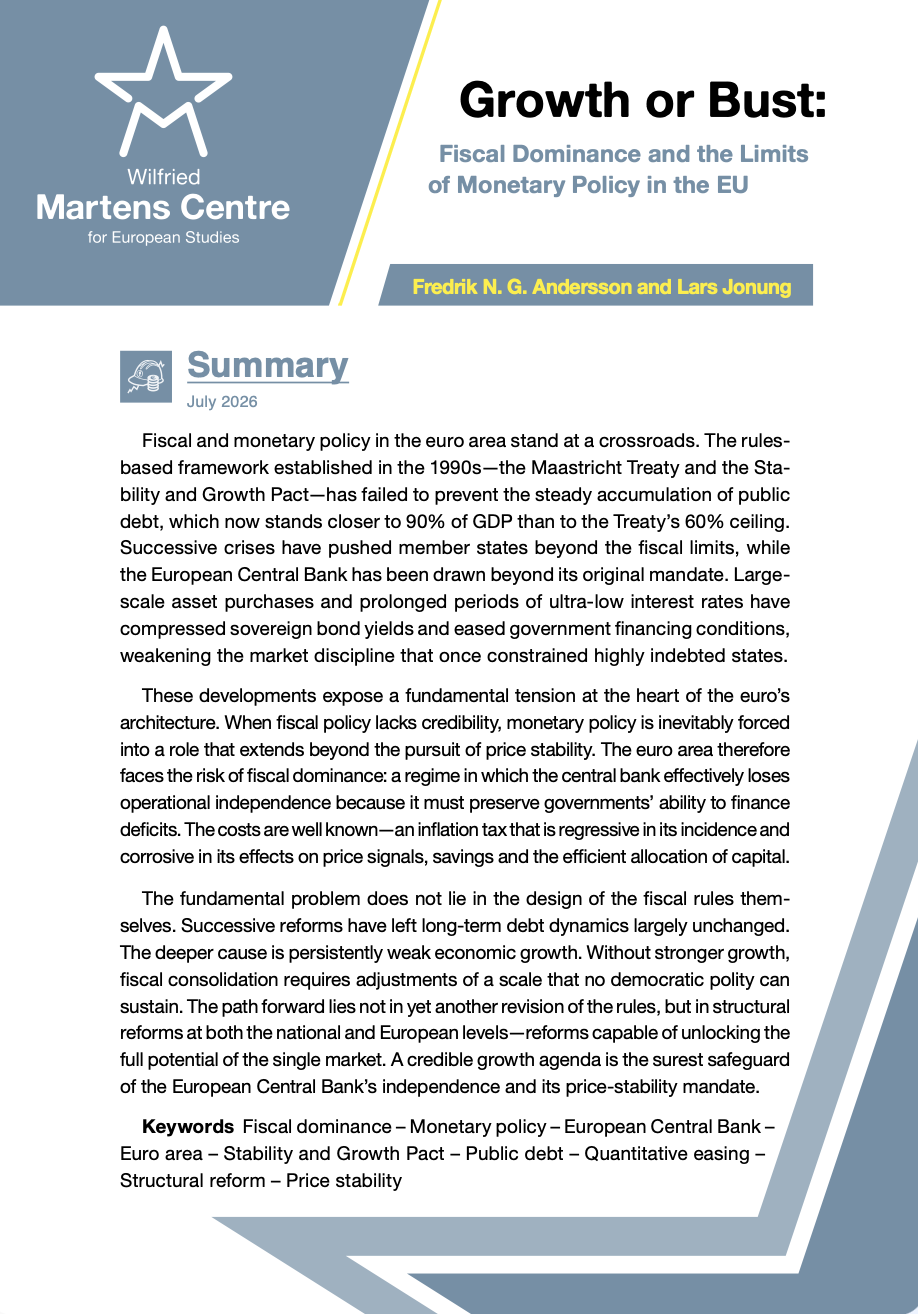

Growth or Bust: Fiscal Dominance and the Limits of Monetary Policy in the EU

-

Policy Briefs

Old, Rich and Afraid: Five Ways to Drive Cultural Change and Deliver a Real European Investment Union

-

Policy Briefs

The Sovereign Isle: Lessons From the UK Economy for the EU’s Future

-

Other

Affordability and Opportunity: How to Heal a Divided Society

-

Other

A reform agenda for the single market

-

Other

Sino-Russian Economic Relations: Dispelling the “No Limits” Partnership Myth

-

Other

Working Migrants Valued for Their Economic Contribution

-

Other

Strategic Policy Recommendations for the European People’s Party