Related publications

-

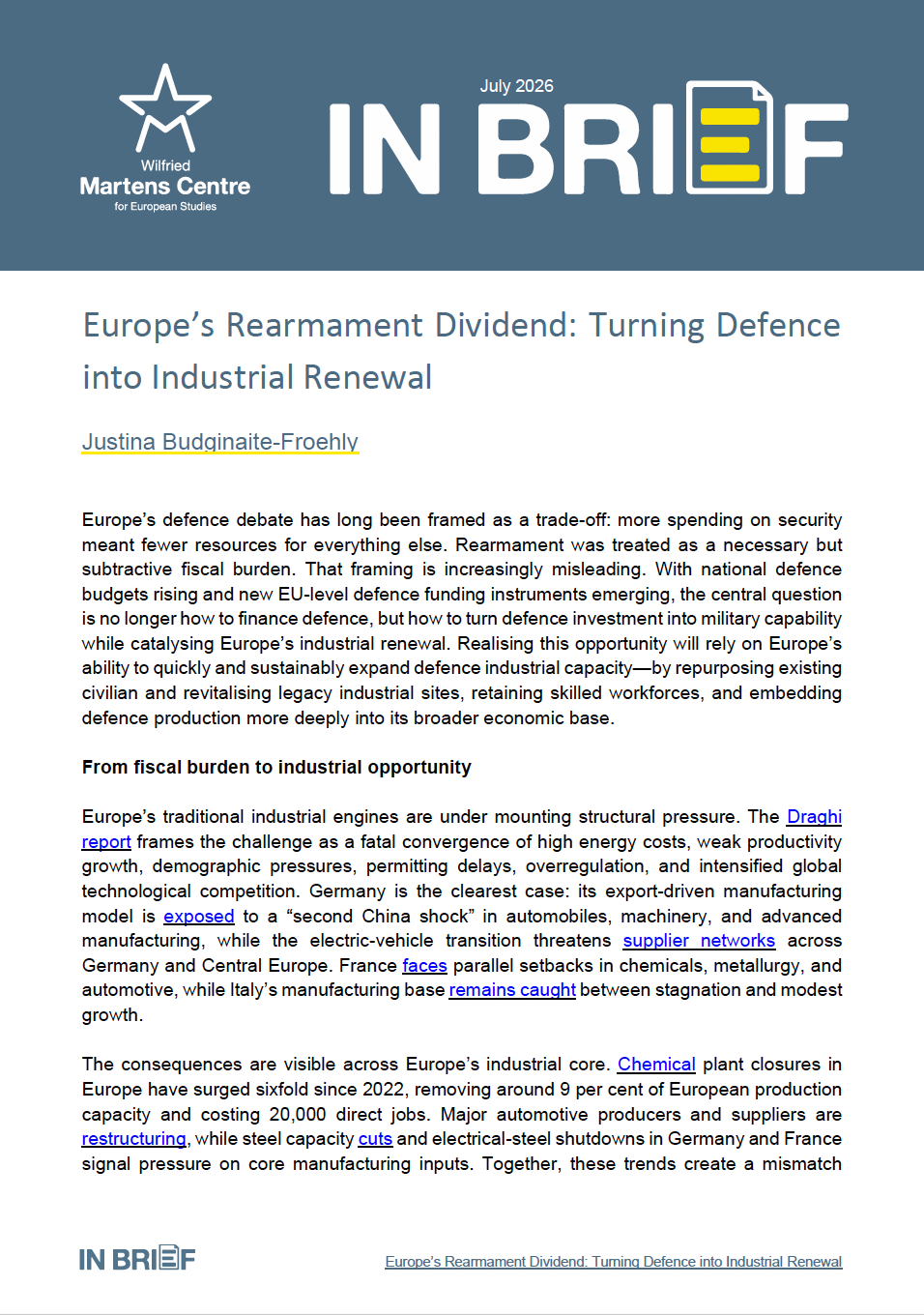

IN BRIEF

Europe’s Rearmament Dividend: Turning Defence into Industrial Renewal

-

Research Papers

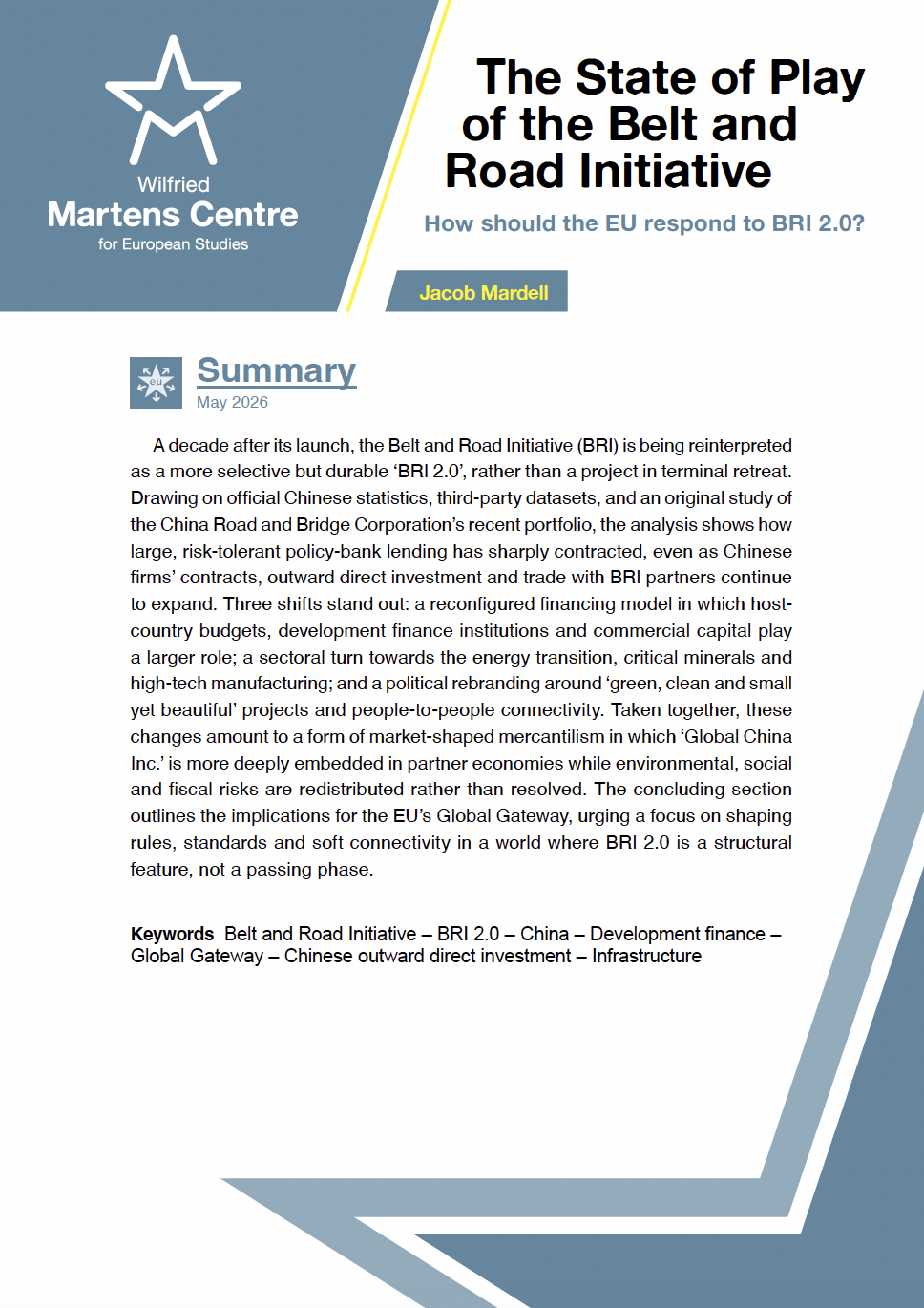

Made in China, Powered by Europe: Mapping the EU’s Strategic Leverage Over the People’s Republic of China

-

Other

Strategic Autonomy Requires a Strategic Partner: Why Europe Must Expand Industrial Cooperation with Taiwan

-

Other

Sino-Russian Economic Relations: Dispelling the “No Limits” Partnership Myth

-

Collaborative

Navigating Multipolarity: Southeast Europe in the EU’s China Strategy

-

Other

From Taiwan to Malaysia: The Silicon Alley of the East

-

Other

Is Draghi Right? Designing the Way Forward

-

Policy Briefs

China’s Electric Vehicle Challenge to Europe: Red Flags and Red Lines